Ever lower rates for the foreseeable future?

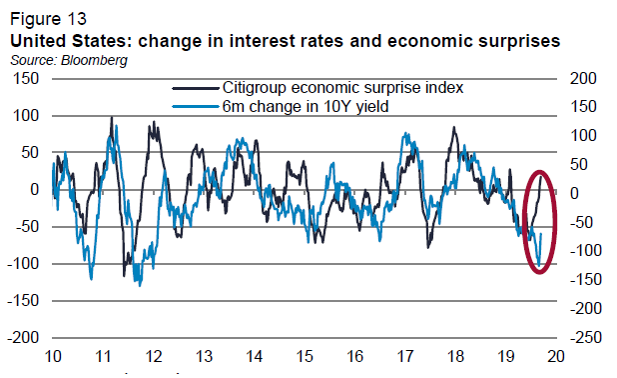

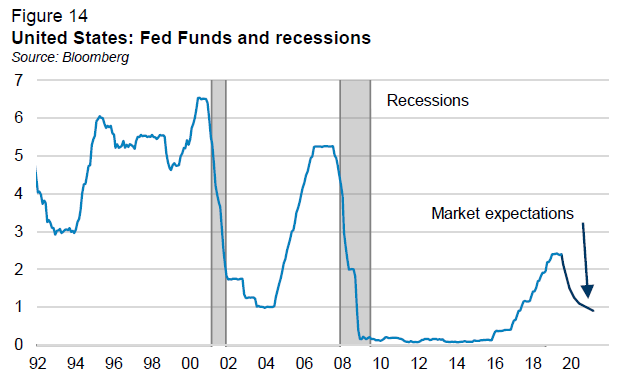

In contrast with wath we were expecting at the start of 2019, US interest rates have fallen steeply this year and are ‘out of sync’ with recent economic trends. Rather than aiming at countering an economic recession, the fall in rates appears to be a shift in monetary policy towards a more accommodative stance structurally.

We believe market expectations for several rate cuts in the US are excessive and if global risks recede to normal levels, then government bond valuations will be penalised. Economic fundamentals could also provoke higher US rates. Core inflation has been ticking up for several months and the budget deficit is still on the rise.

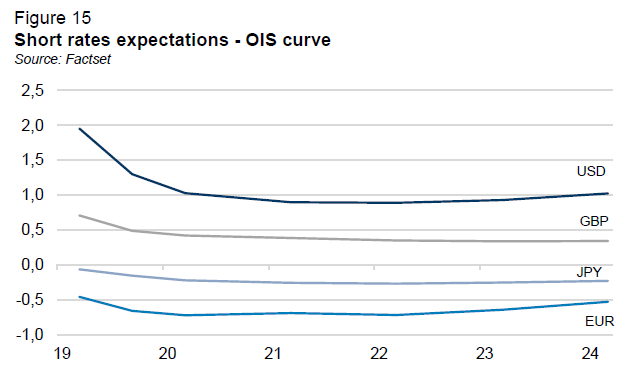

In the eurozone, the ECB’s announcements in September signalled its intention for monetary policy to remain accommodative. The central bank’s new package includes a 10 bps cut in the benchmark deposit rate to -0.50%, a partial exemption mechanism to cushion the negative effects of this measure on banks’ earnings, a relaunch of QE amounting to €20 billion per month for an unlimited period, an extended maturity for the new TLTRO operations, and stronger forward guidance by linking interest rate changes to inflation.

Broadly speaking, markets do not expect monetary policy to normalise in the major developed economies for several years, which will result in profound changes for bond markets.

Towards a new asset class hierarchy?

The nature of the bond market has fundamentally changed. Term premia are now negative and a third of global bond volumes now trade at negative rates. This means that duration will no longer be a performance driver and interest rates will have to head lower in order to ensure positive gains.

Steep falls in long-end bond yields have contributed to the higher risk premia seen across equity markets. The performance gap between equities and government bonds will likely be significantly higher in the future than was the case until now.

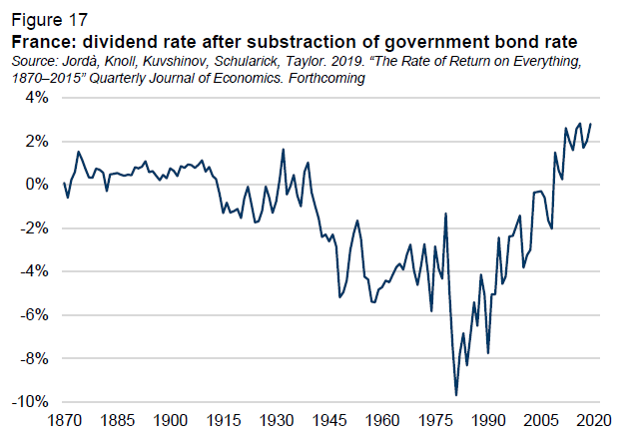

Investors seeking income are now turning to equities as the most attractive asset class, with dividend yields outstripping those of government bonds.

Short-term outlook for risky assets

Equity markets currently offer record-high risk premia compared with other asset classes, more than compensating for their level of risk. An economic recession would be extremely negative for equities but, as things stand, we believe this to be an unlikely scenario.

In terms of equities, we prefer Western markets. Although certainly more expensive than their emerging-market and Japanese counterparts, those in the United States and eurozone are delivering better returns.

In terms of fixed income, we prefer subordinated financial bonds. The additional yield is attractive and these securities should do well if interest rates move higher, as profitability in the financial sector can also be expected to improve.

Credit spreads on high yield bonds are in line with fundamentals, whereas spreads on high quality names are probably too tight to compensate for any rise in interest rates.

In short, we believe current economic conditions are favouring risky assets. We do not see a recession scenario forming in the short term and with the US election now on the horizon, we are more likely to see policies geared towards boosting the economy and markets. Remaining flexible will nonetheless be the best way to navigate global uncertainty.

Glossary:

Term premium: The additional amount that investors receive for duration risk, which in turn is linked to the average life of the bond.

Risk premium: The return in excess of the risk-free rate that an investment is expected to yield.

See also : Video | Economic and market outlook S2 2019

The opinion expressed above is dated September 2019 and is liable to change. Latest available data is used.

This document is not pre-contractual or contractual in nature. It is provided for information purposes. The analyses and descriptions contained in this document shall not be interpreted as being advice or recommendations on the part of Lazard Frères Gestion SAS. This document does not constitute an offer or invitation to purchase or sell, nor an encouragement to invest. This document is the intellectual property of Lazard Frères Gestion SAS.