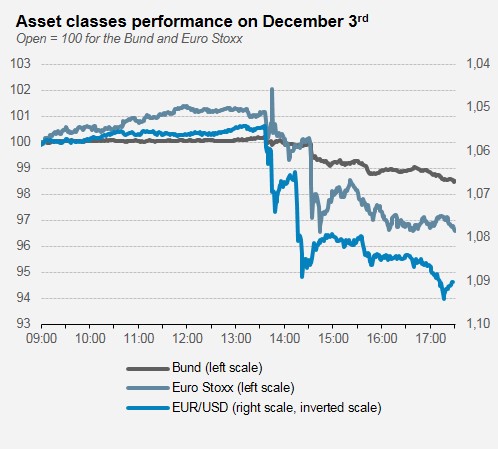

A cut in the ECB’s deposit facility rate to minus 0.3%, a six-month extension of its asset purchase programme March 2017, reinvestment of the principal payments and inclusion of regional and local debt among the eligible assets: in announcing these measures [on Thursday], Mario Draghi doused market expectations. Equities have tumbled, while both the euro and bond yields have surged.

During his press conference, Mr Draghi was at pains to emphasise the euro area’s economic recovery and improved credit conditions. As grounds for the latest measures, he cited slight adjustments to ECB staff projections – upwards in the case of growth, downwards in the case of inflation. He also stuck to his highly dovish bias, making it clear that further easing was on the cards if inflation were to miss the central bank’s target.

What prompted such an extreme market reaction was disappointment. Expectations had been steadily mounting in the preceding days, as analysts seemed to be outbidding each other with ever bolder forecasts. Market participants had apparently convinced themselves that Mario Draghi always went further than anticipated, so they were gearing up for another big bazooka.

But even as the ECB President’s statements since September led investors to expect a fresh bout of stimulus, figures like Benoît Coeuré – by no stretch of the imagination a monetary hawk – were raising questions about how necessary that really was. Apparently, such voices don’t carry as much as Mr. Draghi’s does. The ECB decision was not unanimous, suggesting a particularly stormy rate-setting meeting. So are we dealing here with a problem of miscommunication (with the ECB having a hard time damping market expectations)? Or is the latest policy move the result of gridlock on the bank’s Governing Council (with some of the Governors unwilling to give in to Mario Draghi across the board)?

The meeting’s minutes – scheduled for publication in a few weeks – are likely to make for instructive reading.

But in any case, what we consider worth stressing is that euro area fundamentals are still pointing in the right direction. PMI indices haven’t even blinked despite concerns over the global economy; the unemployment rate shows further decline; and lending conditions have continued to get easier, as the latest ECB figures show. Although the euro has just shot up, it has yet to reach its level of last summer, and we believe that as soon as the Fed starts lifting its rates, the common currency will be in for more downward pressure. In addition, the ECB is poised to step in if required. Taking a step back from the market’s knee-jerk reaction, we believe that the outlook for eurozone equities remains bright.

This document is not pre-contractual or contractual in nature. It is provided for information purposes. The analyses and descriptions contained in this document shall not be interpreted as being advice or recommendations on the part of Lazard Frères Gestion SAS. This document does not constitute an offer or invitation to purchase or sell, nor an encouragement to invest. This document is the intellectual property of Lazard Frères Gestion SAS.